Scroll all the way down to see how huge the nationwide debt could recover from the following few a long time, after which examine how we received right here.

When President Joe Biden delivered his 2023 State of the Union handle, Washington was drowning in a sea of crimson ink. The annual finances deficit was within the means of doubling from $1 trillion to $2 trillion in a single 12 months as a result of some student-debt cancellation shenanigans. That 12 months’s finances deficit would turn into the biggest share of gross home product (GDP) in American historical past exterior of wars and recessions. Economists on the Congressional Budget Office (CBO) and throughout the political spectrum warned that persevering with to disregard the escalating Social Safety and Medicare shortfalls whereas additionally opposing new broad-based taxes was unsustainable and will deliver a painful debt disaster.

How did the nation’s highest elected officers reply to this financial problem? Biden promised that “if anybody tries to chop Social Safety [or] Medicare, I am going to cease them. I am going to veto it.” He additionally accused congressional Republicans of plotting to reform these packages—prompting outraged shouts from Republicans who resented the accusation of caring concerning the looming insolvency of the Social Safety and Medicare belief funds. When the president triumphantly taunted that such boos reveal a brand new bipartisan consensus to do nothing about Social Safety and Medicare shortfalls, each Republicans and Democrats leaped to their toes with thunderous cheers. For good measure, each events endorsed Biden’s prohibition on any new taxes for 95 % of households. Washington’s harmful borrowing spree would proceed with enthusiastic bipartisan assist.

Paradoxically, the quicker authorities debt escalates towards an inevitable debt disaster, the much less politicians and voters appear to care. Within the Eighties and Nineteen Nineties, extra modest deficits dominated financial coverage debates and prompted six main deficit reduction deals that balanced the finances from 1998 by way of 2001. That period is lengthy gone. Up to now eight years, President Donald Trump after which Biden enacted $12 trillion in deficit-expanding laws at the same time as Social Safety and Medicare shortfalls drove baseline deficits larger. When even liberal economists warned politicians that the post-pandemic economic system confronted a modest diploma of rising inflation and rates of interest—and {that a} federal spending spree would pour gasoline on that fireplace—lawmakers responded by enacting the $2 trillion American Rescue Plan. When inflation and mortgage charges resultantly surged to 9.1 percent and 7.8 percent, respectively, lawmakers openly continued the inflationary spending spree.

Why are we not responding to hovering debt and its financial penalties? Whereas there are lots of elements, the three most essential are these: 1) We have satisfied ourselves that deficits don’t matter; 2) partisan politics and the collapse of lawmaking have turned deficits right into a weapon to be politicized fairly than an issue to be solved; and three) few of us are keen to face the unpopular actuality that this challenge can’t be resolved with out basically reforming Social Safety, Medicare, and middle-class taxes.

Debt Drivers

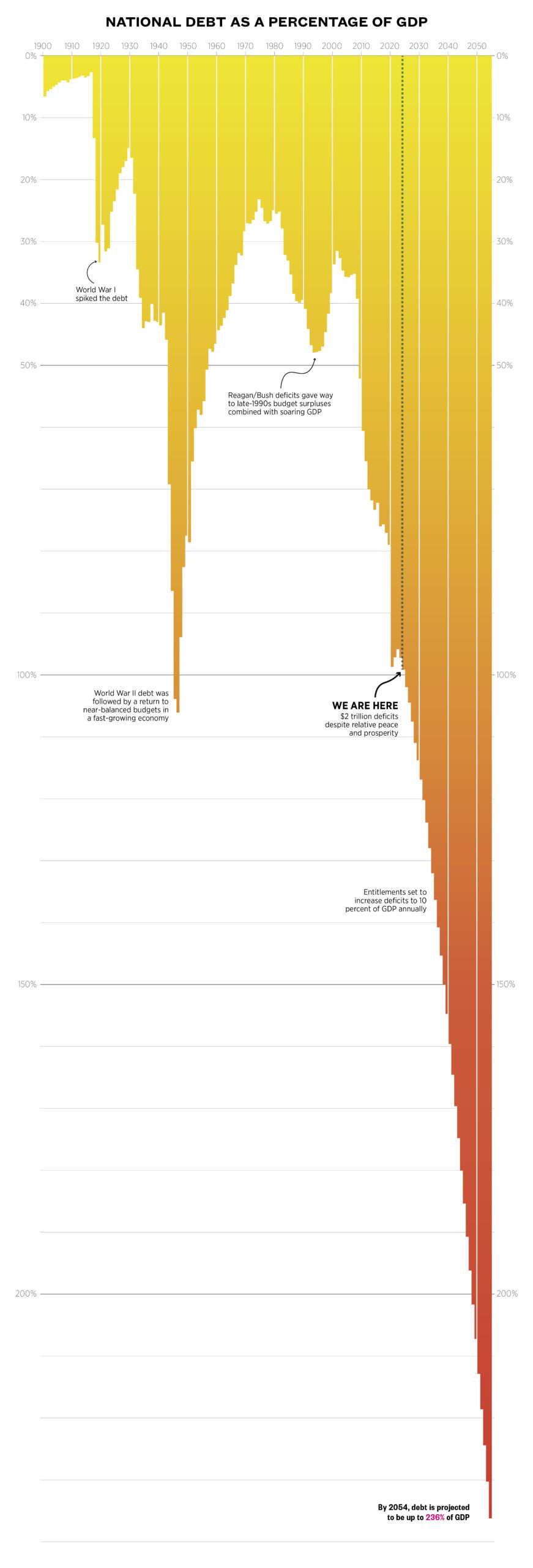

Few voters, and even politicians, have totally grasped how perilous Washington’s fiscal outlook has turn into. Whereas finances deficits have traditionally averaged 3 % of GDP—making certain the debt grows no quicker than the general economic system—the deficit reached 7.5 % of GDP final 12 months and is projected to swell to 14 % of GDP over three a long time if present tax and spending insurance policies are prolonged. If the federal debt continues to roll over into the 4.5 % rate of interest seen at current Treasury debt auctions, then the finances deficit could surpass $4 trillion inside a decade.

When a debt turns into this monumental, rates of interest turn into a budgetary time bomb. Even when charges keep under 4 % ceaselessly—because the CBO’s projections questionably assume—projected curiosity prices will devour 1 / 4 of all federal taxes inside a decade and turn into the biggest annual federal expenditure within two decades. If charges rise, every proportion level will add $35 trillion in curiosity over three a long time—the price of including one other Protection Division. Once more, that is for every proportion level.

To many economists, a very powerful debt determine is the whole federal debt as a share of the economic system. This “debt ratio” has already leapt from 40 % to one hundred pc since 2008, and it’s projected to exceed 230 % inside three a long time below present insurance policies. If rates of interest steadily rise to five % and even 6 %, the debt ratio might surpass 300 %, with curiosity prices consuming almost all annual tax revenues. There can be no tax revenues left to finance any federal packages.

If this sounds unduly alarmist, take into account that the economists on the College of Pennsylvania’s Wharton Faculty couldn’t even undertaking a functioning long-term economic system on our present debt path. The economists write that their financial fashions “successfully crash when attempting to undertaking future macroeconomic variables below present fiscal coverage. The reason being that present fiscal coverage shouldn’t be sustainable and forward-looking monetary markets comprehend it.”

The motive force of this debt isn’t any thriller. The mix of rising well being care prices and 74 million retiring child boomers is driving annual Social Safety and Medicare prices far above their payroll tax and Medicare premium revenues. These annual program shortfalls—which should be funded with normal tax revenues and new borrowing—will exceed $650 billion this 12 months on their strategy to $2.2 trillion yearly a decade from now, when together with the curiosity prices of their deficits. Particularly, by 2034 Social Safety and Medicare can be amassing $2.6 trillion yearly in revenues whereas costing $4.8 trillion in advantages and related curiosity prices.

And that is just the start. Over 30 years, CBO data present Social Safety and Medicare going through an annual shortfall of $124 trillion whereas the remainder of the finances is roughly balanced. By 2054, these two packages can be contributing 11.3 % of GDP to annual finances deficits, or the present equal of $3.2 trillion in annual program shortfalls (together with the curiosity prices of their deficits). As for the remainder of the finances, CBO projects that tax revenues will proceed to rise, and different program spending to fall, as a share of the economic system. This implies the whole long-term deficit progress is pushed by Social Safety, Medicare, and the curiosity price of their shortfalls.

Child boomer retirements, well being care prices, and rising rates of interest mix to create what Invoice Clinton’s former White Home chief of workers, Erskine Bowles, in 2012 called “probably the most predictable financial disaster in historical past.” Way back to the 1990s, specialists warned that surging retirements within the 2010s and 2020s would push Social Safety and Medicare prices dangerously far above their more-steady payroll tax revenues. But makes an attempt within the Nineteen Nineties and early 2000s to steadily section in reforms whereas the boomers had been nonetheless younger sufficient to regulate to them went nowhere. Consequently, stabilizing the debt will now entail deeper and extra drastic Social Safety and Medicare reforms—in addition to will increase in middle-class taxes—that may not exempt present and close to retirees.

We can’t grandfather out of reform the 74 million boomers whose prices are driving the $124 trillion shortfall. Nor can we tweak our manner out of this. If the system is to be stored afloat, Social Safety’s eligibility age must rise, its profit progress formulation should be considerably curtailed for above-average earners, and its taxes could have to rise too. Medicare premiums should steeply rise for above-average earners, and its elevated prices addressed both with a brand new choice- and competition-based premium support system or with bold value and cost reforms to cut back pricey procedures.

Washington is not going to even focus on this.

Deficits Do Matter

Youthful voters could not grasp how a lot deficit considerations dominated financial coverage debates from 1982 by way of the top of the century. As deficits widened below President Ronald Reagan, as a result of tax cuts and navy spending, deficit discount grew to become a prime voter precedence, pushed by considerations of elevated rates of interest, sluggish financial progress, and international debt possession. These deficit considerations—coloured by a modest recession—helped elect President Invoice Clinton in 1992. In The Agenda, Bob Woodward detailed the Clinton White Home’s monomaniacal give attention to finances deficits, rates of interest, and the bond market when pushing its 1993 tax hike invoice. Even with the debt roughly steady as a share of the economic system, each events demanded aggressive deficit discount to chop rates of interest, spur funding, and encourage financial progress.

After six main deficit discount offers and a short lived income surge lastly introduced balanced budgets from 1998 by way of 2001, triumphant lawmakers shifted the controversy to learn how to spend $5 trillion in projected (and, on reflection, fake) 10-year surpluses. At the same time as a sluggish economic system eradicated these surpluses, Washington’s urge for food for changing austerity with tax cuts, warfare spending, and new entitlements couldn’t be stopped. Vice President Dick Cheney famously declared “deficits do not matter”—and when Nice Recession stimulus spending introduced the primary trillion-dollar deficits with none instantly obvious hazard, all of Washington wished to hitch the occasion. Low rates of interest made federal borrowing low-cost, and the 2016 and 2020 presidential campaigns noticed Sen. Bernie Sanders (I–Vt.) suggest between $60 trillion and $97 trillion in new spending over a decade. Then Presidents Trump and Biden enacted $12 trillion in deficit-financed laws in simply eight years.

Progressives even invented an absurd justification for huge deficits. Fashionable Financial Concept (MMT) inexplicably claimed that Scandinavian-size spending may very well be financed by radically increasing the cash provide with out vital inflation. The 72 main economists on the left and proper responding to an expert survey unanimously rejected the MMT’s ahistorical and nonsensical claims. The MMT’s actual objective was to concoct an financial justification for progressives’ longstanding want to drastically increase authorities unconstrained from the bounds of believable taxation.

In hindsight, the economic system managed the post-2000 debt surge as a result of the preliminary 32 % of GDP debt degree supplied some fiscal house for extra borrowing. Moreover, the sluggish economic system, an accommodating Federal Reserve, and a world financial savings glut drove a historic rate of interest decline that made debt extra reasonably priced for households, companies, and the federal finances.

That free-lunch period is now over. The federal debt exceeds one hundred pc of GDP and is ready to double and even triple over just a few a long time. These debt ranges are rendered much more unaffordable by rising rates of interest, because the structural factors that lengthy diminished charges start to reverse. Consensus financial evaluation suggests that the debt surge itself will elevate rates of interest by as a lot as three proportion factors.

Sadly, American politics has not caught as much as this new financial actuality—which brings us to one of many largest limitations to reform.

Partisan Politics and the Collapse of Lawmaking

Washington was not all the time as hyperpartisan and dysfunctional as it’s right this moment. In 2019, I analyzed the 14 main “grand deal” deficit negotiations from 1983 by way of 2019 to be taught why six negotiations efficiently enacted laws and eight failed. Crucial explanation for the current failures, I discovered, has been Congress itself.

Up by way of the mid-Nineteen Nineties, Republicans and Democrats—regardless of public bickering—typically collaborated effectively behind the scenes. Through the 1983 Social Safety negotiations to avert a looming trust-fund insolvency, Reagan and Home Speaker Tip O’Neill (D–Mass.) pledged to not assault one another’s approaches in public. President George H.W. Bush and congressional Democrats trusted one another within the 1990 finances deal negotiations that introduced new spending controls and tax will increase. Even the 1997 balanced finances settlement between Clinton and Home Speaker Newt Gingrich (R–Ga.), coming two years after a rancorous authorities shutdown, was a model of wholesome, reliable, bipartisan negotiations.

This bipartisan period ended abruptly in January 1998, when the Clinton-Lewinsky scandal broke. Clinton and Gingrich canceled a bipartisan repair to Social Safety that was set to be introduced simply days later. Deficit considerations didn’t return till 2009, and by then Washington was much more polarized.

Reasonably than keep in D.C. in the course of the legislative session and construct bipartisan relationships—which voters as soon as rewarded—lawmakers now fly into Washington on Monday night, assault the opposite occasion in press releases and flooring speeches, after which fly out on Thursday afternoon. The media panorama has turn into fragmented, partisan, paranoid, and obsessive about narratives of betrayal. Gerrymandered Home districts depart members extra frightened of major challenges from true-believing partisans than of dropping swing voters within the normal election. Most congressional coverage making has been faraway from comparatively bipartisan congressional committees and centralized within the Capitol workplaces of the Home and Senate occasion leaders.

The result’s 24/7 partisan warfare, with particular person points seen as little greater than interchangeable weapons within the day’s communication wars. For the previous two years, Republicans and Democrats savaged one another over inflation—the voters’ prime challenge—with out both aspect bothering to supply critical laws to resolve the issue. (The cynically named “Inflation Discount Act” had little to do with combating inflation.) On this surroundings, neither occasion dares to push politically dangerous entitlement reforms or broad-based taxes. Simply ask former Home Speaker Paul Ryan (R–Wisc.), whose earlier efforts earned him bipartisan hatred from voters and an attack ad portraying him murdering a senior citizen.

Even when the events might belief one another to barter a good-faith deficit deal, their very own purity-test voters would accuse them of surrendering to the opposite aspect. So Republicans and Democrats simply level fingers at one another. Deficits aren’t an issue to be solved, however as a substitute one other weapon within the partisan communications warfare.

No Extra Straightforward Options

Within the Eighties and ’90s, lawmakers might tweak their strategy to deficit discount. Almost half of federal spending was discretionary, and the Chilly Conflict victory introduced huge navy savings that minimized the necessity for austerity elsewhere. A late-Nineteen Nineties revenue bubble was sufficient to bump the deficit into surplus for 4 years. The political payoff of a balanced finances was value these modest reforms.

In the present day’s deficits of $2 trillion—headed towards $3 trillion and even $4 trillion—can’t be tweaked away. Balancing the finances is nearly not possible, and even stabilizing the long-term debt at right this moment’s one hundred pc of GDP requires wildly unpopular modifications to Social Safety and Medicare (and can seemingly take broad-based taxes). Different reforms are obligatory however removed from adequate.

But Washington refuses to confront this finances math, relying as a substitute on publicity stunts. Voters seek for “one cool trick” that may rapidly and painlessly stability the finances if solely the out-of-touch politicians would pay attention.

Begin with Republicans. The GOP canon begins by asserting that deficits are all the time pushed by Democratic spending. This narrative is flatly contradicted by Presidents George W. Bush and Trump, each of whom expanded federal spending by trillions of {dollars} whereas enacting trillion-dollar tax cuts. The final time Republicans managed each the White Home and Congress, in 2017 and 2018, they instantly lower taxes by $1.5 trillion, expanded discretionary spending by 13 percent in a single 12 months, and rejected all entitlement financial savings.

“However these tax cuts paid for themselves,” Republicans retort, which incorrectly assumes that pre-cut tax charges are all the time above the Laffer Curve’s revenue-maximizing fee. This math additionally requires that each tax lower greenback provides a minimum of $5 in financial output, taxed at a mean 20 % fee to recuperate that misplaced income greenback. Whereas tax cutters will level to rising tax revenues as proof of “free” tax cuts, even a steady tax code will produce rising revenues as a result of inflation, inhabitants progress, rising actual wages, and enterprise income. Regardless of the various constructive attributes of GOP tax cuts, they undeniably resulted in decrease tax revenues than in any other case.

On the spending aspect, Republican voters are fast to say {that a} $2 trillion deficit may be largely eradicated by chopping international help (simply 1 % of federal spending) or the basic “waste, fraud, and abuse,” as if such a line-item exists within the federal finances to be zeroed out. Some Republicans like to speak about eviscerating social spending, however that rhetoric tends to crumble while you calculate how a lot of that spending you’d want to chop to fulfill the GOP’s balanced-budget targets: You’d have to eradicate all funding for veterans’ advantages, youngster credit score funds, the earned revenue tax credit score, college lunches, incapacity advantages, Okay-12 education, well being analysis, unemployment advantages, meals stamps, homeland safety, infrastructure, embassy safety, federal prisons, border safety, and rather more. There’s not a lot Republican urge for food for that. (And no, immigration doesn’t considerably widen federal finances deficits, though it may well increase state and native authorities prices.)

GOP leaders additionally depend on gimmicks. Trump absurdly guarantees to repay the $27 trillion federal debt with oil and fuel revenues. One current Republican presidential candidate, Vivek Ramaswamy, promised to develop the economic system to a balanced finances. That lazy competition not solely requires almost not possible progress charges; it fails to acknowledge that quicker financial progress additionally raises Social Safety and Medicare prices and rates of interest on the federal debt.

And not using a consensus round a critical deficit discount agenda, many Republicans rely as a substitute on gimmicks and publicity stunts. So-called government shutdowns have an effect on lower than a tenth of federal spending, eviscerate most of the hottest packages, and assure an intense voter backlash. Equally, debt limit showdowns offend voters as a crude manner of eliminating an undetermined quarter of federal spending, defaulting on federal contract funds, and probably defaulting on the debt with devastating financial penalties. They by no means succeed.

One other Republican gimmick is just to demand a balanced finances modification, or easy-sounding spending caps such because the “Penny Plan,” with out specifying learn how to meet their impossibly tight financial savings targets. Empty lawmaker pledges to rapidly stability the finances whereas additionally extending the 2017 tax cuts and defending key spending priorities—a mathematical and political impossibility—are supposed to distract conservative voters from their runaway spending. Discuss like Barry Goldwater; spend like LBJ.

So George W. Bush signed laws collectively including $6.9 trillion in debt, whereas Trump signed $7.8 trillion in simply 4 years. The Home GOP’s balanced finances plan consists almost fully of gimmicks. Lawmakers interact in symbolic fights over small slivers of discretionary social spending whereas entitlement prices skyrocket. Freedom Caucus lawmakers give indignant press conferences demanding colossal spending cuts with out bothering to put out any particular financial savings blueprint to fulfill their calls for—or doing the required outreach, negotiating, and coalition constructing to win over skeptical lawmakers. It is all only a present; performative outrage for gullible voters.

Democrats have additionally constructed their very own bubble of misinformation and excuses. Essentially the most fundamental progressive narrative claims that deficits don’t matter and are merely a green-eyeshade scheme to serve the rich over the individuals. These progressives provide no reply for who will lend Washington a minimum of $120 trillion over 30 years, or how such debt will have an effect on the economic system. The MMT lovers name for financing such deficits with new cash creation after which faux hyperinflation wouldn’t outcome. “Zombie Keynesians” assert that trillions of {dollars} in deficit spending is required to maintain the economic system afloat, and that even slowing the expansion of spending would deliver recession, mass poverty, and social collapse. (Actual Keynesians acknowledge that recessionary stimulus additionally requires offsetting austerity throughout financial expansions.)

Liberal Democrats all of a sudden turn into anti-deficit when hammering Republicans. Flipping the GOP argument, they assert that Republicans drive the debt as a result of deficits expanded throughout current Republican presidencies and declined below Democrats. But such arguments measure solely the primary and final years of every presidency, which are sometimes closely affected by one- to two-year fiscal anomalies exterior of presidential management, such because the 2000 income bubble, the 2008 housing crash, and the 2020 world pandemic. The truth is, the partisan impact on deficits disappears if you happen to measure deficits throughout complete presidencies, management for elements which can be inherited or exterior presidential management, and incorporate the partisan make-up of Congress passing the finances payments. Sadly, these commonplace financial and statistical cleanups don’t slot in a meme.

Maybe probably the most persistent Democratic fantasy is that tax cuts for the rich brought about right this moment’s deficits and that taxing the wealthy can eradicate the issue. The maths simply does not again this up. Annual federal budgets since 2000 have fallen from a 2.3 % of GDP finances surplus to a 7.5 % of GDP deficit. That 9.8 % decline results from annual spending leaping 6.3 % of GDP; the bursting of the 2000 income bubble, which diminished revenues by 1.5 % of GDP; and tax cuts, costing 2 % of GDP. Roughly 70 % of the 2001 and 2017 tax lower prices (and subsequent extensions) went to earners within the center and decrease courses. Out of that 9.8 % of GDP fiscal decline, that leaves simply 0.6 % that may be attributed to “tax cuts for the wealthy.”

So how do critics declare that “tax cuts for the wealthy” drive deficits? By together with all tax cuts even for the nonwealthy. Or just giving a free cross to the 5.5 % of GDP entitlement spending hike since 2000 after which blaming tax revenues for not maintaining.

In its extra excessive type, this fiscal fallacy insists that merely taxing the wealthy can’t solely shut between $120 trillion and $150 trillion (relying on present coverage extensions) in complete finances deficits over three a long time, but in addition finance a full Nordic social democracy. The primary drawback with this declare is mathematical. Even seizing every dollar of wealth from America’s 800 billionaires—each residence, yacht, enterprise, and funding—would merely fund the federal authorities for 9 months. After which the cash can be gone. So would your 401(okay), given that the majority of this wealth can be seized from the inventory market. Not even the Sanders fantasyland tax agenda of a 77 % property tax, 8 % wealth tax, and large company, revenue, and funding taxes might finance Washington’s present spending guarantees, a lot much less his monumental new spending agenda. There merely are not enough millionaires, billionaires, and undertaxed firms to shut a minimal $120 trillion shortfall or finance a beneficiant social democracy for 330 million Individuals.

The second drawback is financial. Solely so many upper-income taxes may be layered on prime of one another earlier than surpassing their revenue-maximizing charges. At most, 1 % to 2 % of GDP in new taxes may very well be raised from excessive earners and firms earlier than their tax charges attain revenue-maximizing ranges and the economic system begins to capsize.

The ultimate drawback is political. Even a unified, unconstrained Democratic authorities in 2021 and 2022 restricted its tax-the-rich attain to a modest and exception-stuffed company minimal tax and a few IRS funding. It seems that numerous excessive earners and firms are situated in California and New York, the place they assist elect Democratic congressional leaders, who aren’t wanting to bury them in a socialist tax revolution.

Progressive lawmakers exaggerate tax-the-rich financial savings by recycling the identical few tax proposals to pay for numerous spending proposals. Liberals lionize the 91 % revenue tax charges of the Fifties, with out doing the basic research to find that: 1) Just about no one in these days truly paid marginal tax charges over 50 %; 2) these excessive earners paid decrease efficient charges than right this moment; and due to this fact 3) the excessive tax charges of the Fifties to Nineteen Seventies collected a smaller share of GDP in revenues than the post-1980 period of considerably decrease tax charges. And when tax-the-rich progressives name for matching Europe’s larger tax revenues, they ignore the truth that nearly all of Europe’s income benefit results from broad-based value-added and payroll taxes, not further upper-income taxes. Taxing the wealthy needs to be on the desk—as ought to all financial savings insurance policies—however can’t shut greater than a modest fraction of the shortfalls.

Democrats provide different doubtful simple options to deficits. The favored goal of Pentagon spending has already fallen from 6 % to three % of GDP for the reason that Eighties and is projected to continue declining to 2.5 %, which isn’t far above NATO’s 2 % goal. Furthermore, congressional calls to dramatically slash navy spending haven’t been backed up by specific proposals, as a result of even progressive lawmakers can’t work out learn how to meet their financial savings targets.

Equally, Medicare for All is extra of a speaking level than a critical financial savings proposal. Payments from Sanders and Rep. Pramila Jayapal (D–Wash.) promise almost not possible effectivity financial savings but fail to specify any new supplier cost system to attain them. As a substitute, the payments lamely assign another person to determine learn how to make all of it work. In the meantime, economists estimate that any modest effectivity financial savings can be spent on expanded advantages, leaving nationwide well being expenditures largely unchanged. Moreover, nobody has but designed a “Medicare for All” tax massive sufficient to interchange the $3 trillion in annual non-public well being spending that may be nationalized. Most crucially, none of those proposals would have an effect on Medicare’s projected $87 trillion three-decade shortfall, as a result of, clearly, old-age Medicare already pays Medicare for All’s decrease supplier charges.

Some myths are bipartisan, similar to claiming that Social Safety and Medicare can’t legally run deficits, that the majority seniors are impoverished, and that retirees accumulate solely as a lot as they paid into the techniques. In actuality, these two packages will run a mixed deficit of $650 billion this 12 months, senior incomes have soared four times as quick as employee incomes since 1980, and most retirees obtain Social Safety and particularly Medicare advantages substantially exceeding their lifetime contributions.

One other fantasy is that the Social Safety belief fund comprises actual assets to pay advantages—or would have if politicians had not “raided it” for different spending. Some declare that long-term Social Safety and Medicare projections are simply guesses, regardless that their retirees exist already with profit formulation set in legislation; or that we will protect everybody over age 50 from reform, regardless that that window closed 20 years in the past.

The media typically encourage pretend options and deficit denial. Bloomberg has hyped the mathematically not possible free-lunch fantasy that billionaire taxes can repair Social Safety. Not surprisingly, it proved standard. Main media organizations criticize runaway deficits however then reply to even modest proposed spending cuts with apocalyptic protection of households who supposedly can be pushed into destitution if their Social Safety advantages develop at a barely diminished fee or their Medicare co-pays rise by just a few {dollars}.

Again to Actuality

Our fiscal lies and myths replicate motivated reasoning as a result of we refuse to confront the inevitable tradeoffs for Social Safety, Medicare, and middle-class taxes. I’ve briefed dozens of lawmakers and a few prime presidential candidates. They’re conscious that the untenable fiscal scenario is heading towards a painful reckoning. However most easily refuse to debate it publicly—and a few even demagogue political opponents who attempt to handle it—as a result of they admit that the brutal politics of deficit discount depart them no selection.

And for that, the voters are guilty. We oppose actual deficit reforms in favor of “one cool trick” gimmicks. We make self-righteous fiscal calls for which can be incoherent, contradictory, and reckless, similar to concurrently calling for a balanced finances, larger spending, and no extra taxes. We vote for Santa Claus candidates of each events who promise a free lunch and reject candidates who acknowledge fiscal tradeoffs. We blame the opposite occasion for deficits and savage any politician who dares to suggest actual reforms. Finally, we’re the rationale that admittedly craven politicians will not danger addressing our looming fiscal insolvency. And we are going to finally pay the worth.

It is time for voters and politicians to confront some inconvenient truths. Washington has promised considerably extra spending than the economic system and tax system will be capable to ship. There is no such thing as a simple answer that everybody missed or that politicians are hiding from you. Washington can’t proceed its present course towards a debt of 200 % and even 300 % of the economic system. The monetary markets will certainly not be capable to lend us between $120 trillion and $150 trillion over three a long time at rates of interest of simply 2 % or 3 %. We have no idea exactly when the monetary markets will faucet out and demand unaffordable rates of interest, making a vicious circle of rising debt and rates of interest. However that day will nearly actually arrive except Congress acts.

This is the painful actuality for Republicans: You can’t stabilize the long-term debt with tax revenues remaining at 18 % of GDP. Federal spending is headed towards 32 % of GDP, as a result of 74 million child boomers retiring into Social Safety and Medicare, rising well being care prices, and debt curiosity bills. You’ll be able to’t merely cancel these prices. Nor are you able to extra aggressively eviscerate standard packages simply to honor a pledge to spare millionaires, billionaires, and firms from one greenback in new taxes. Everybody should contribute. Essentially the most ambitious-yet-plausible conservative reforms would restrict long-term spending to 23 % of GDP, which in flip requires revenues of 20 % to stabilize the debt. This implies bold reforms to Social Safety, Medicare, and protection, in addition to new taxes. Yearly of delay leaves the debt bigger, curiosity prices larger, and getting old boomers much less in a position to take in reforms—forcing a extra tax-heavy eventual answer. Search a compromise now, not later.

This is the painful actuality for Democrats: You can’t chase spending heading to 32 % of GDP with taxes. Even maximizing each tax-the-rich coverage shouldn’t be near sufficient. Nor might deep navy cuts or Medicare for All make a significant dent in deficits heading towards 14 % of GDP. Moreover, middle-class households is not going to settle for their taxes doubling merely to make sure that wealthier child boomer retirees can proceed to gather Social Safety and Medicare advantages far exceeding their lifetime contributions. Neither is it “progressive” to squeeze each remaining progressive funding priority and absorb all believable upper-income taxes merely to subsidize often-wealthy seniors.

And the truth for each events: You want one another. You should put all spending and taxes on the desk to attain the required financial savings, and also you want one another to supply the required political cowl. No occasion is robust sufficient to muscle by way of a partisan, one-sided austerity answer after which survive the brutal partisan onslaught that follows. The political mannequin is the 1983 Social Safety reforms, the place each events held palms, jumped collectively, and had been overwhelmingly reelected.

Crucial reform variable is the voters. Lawmakers is not going to act so long as they concern that even discussing deficit-reduction proposals will provoke a livid backlash. For many years, we have been warned {that a} debt disaster is coming after the boomers retire. With finances deficits exceeding $2 trillion and sure surging previous $3 trillion inside a decade, does anybody care to cease it?

This text initially appeared in print below the headline “The Debt Lies We Inform Ourselves.”